Europe

Loading...

Marketing Communication. Capital at Risk. Professional Investors Only. Please read fund legal documentation before making any final investment decisions.

Just a few years ago, data centres were designed to store files and run everyday software. Today, they are being reimagined from the ground up to function as AI super-factories, running advanced AI workloads round the clock.1 This transformation is not subtle, but rather a structural shift in how these giant computing hubs are designed, where they are built, and what power sources power them.2

One of the key drivers of this shift is the rapid commercialisation of AI we’ve seen over the past few years. Platforms like ChatGPT have grown in a short period of time to attract 800 million weekly users, rivalling top internet platforms in scale.3 New AI products are seemingly launching every day, while query volume is scaling at an unprecedented pace.4 Across customer service, medical diagnostics, logistics, and fraud detection, AI applications are surging into production, seemingly limited only by the availability of AI-tuned computing infrastructure.5

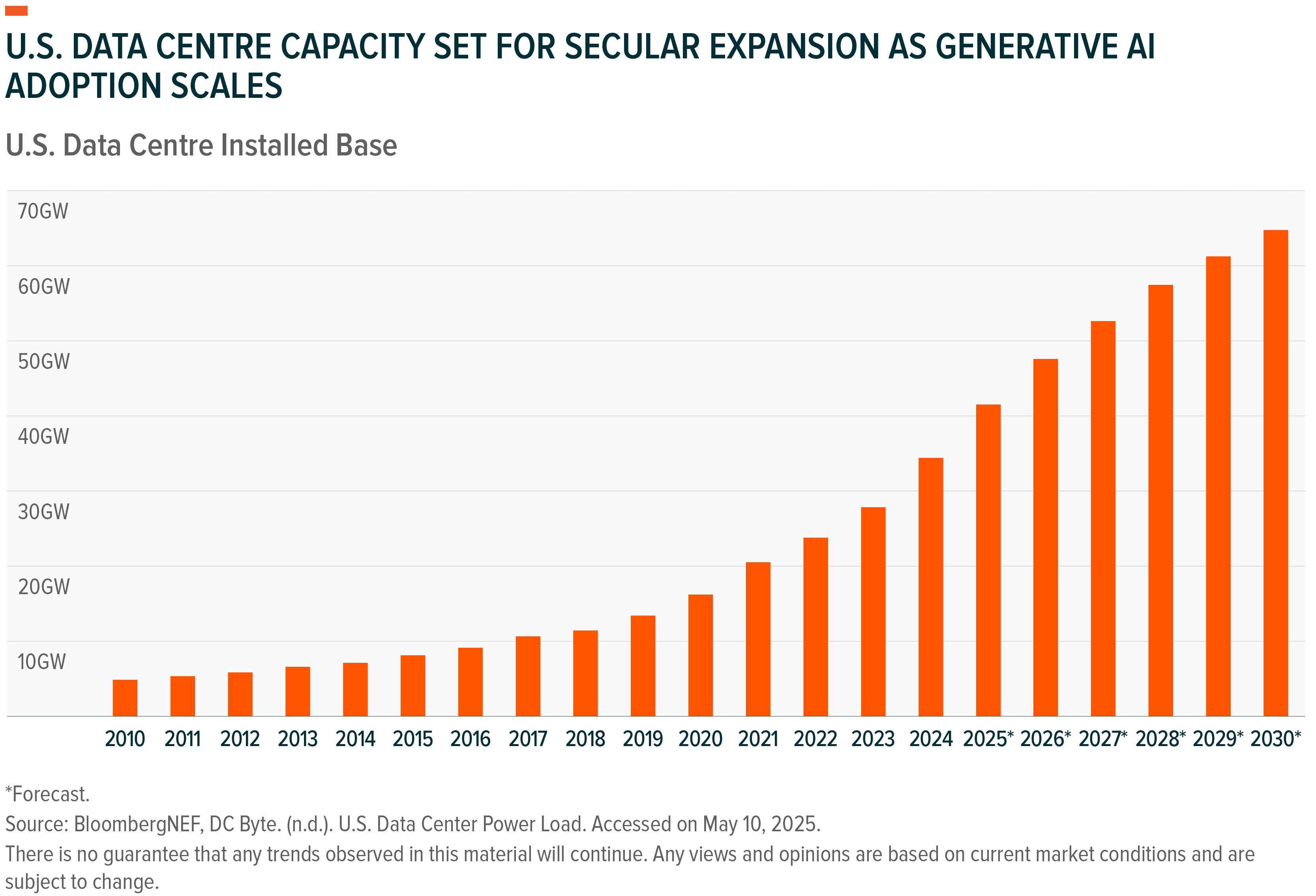

To support this growth in AI computing needs and to enable frontier tech like Physical AI or Quantum Computing, global data centre capacity needs to expand significantly.6

Key Takeaways

Data Centres the New AI Toll Roads?

Over the past decade, data centres were primarily built to handle the surge in data creation and software adoption. Between 2015 and 2025, global data assets surged by 1,258%.9 Global software spending may nearly quadruple.10 Consumers - empowered by 5G, better mobile devices, and the mass digitisation of daily life during the pandemic - were the primary drivers of this buildout. Mobile games, streaming, chat apps, payment apps, and such compounded the trend.11

That dynamic arguably shifted with the arrival of ChatGPT. Conversational AI became the mass market interface almost seemingly overnight, spiking user engagement and pushing large language models to process more data, faster.12 At the same time, users' expectations grew, with queries accompanied by images, videos, and longer context windows, further compounding computing demands and triggering a wave of new AI applications.13 All of this appears to have resulted in unprecedented processing capacity demand that the AI industry hadn’t fully anticipated.14

The industry has responded by investing aggressively and urgently.15 Globally $455 billion was spent on data centres in 2024, up 51% year-over-year YoY.16 And yet, the true scale of power-hungry, latency-sensitive AI compute is potentially beginning to reveal itself as applications remain tightly metered and the availability of AI servers, especially with sufficient power connectivity, continues to be a critical bottleneck.17

From a user-demand perspective, have we just scratched the surface of the opportunity? Only 34% of U.S. adults claim to be users of ChatGPT.18 Beyond that, most users will probably experience conversational AI weightlessly without logging into apps like ChatGPT, as AI it gets integrated into social media platforms, digital maps, productivity software, and smartphones. New paradigms like Agentic AI or Physical AI remain majorly constrained by the availability of computing infrastructure today.19

Scarcity Drives Pricing Power in AI-Era Data Centres

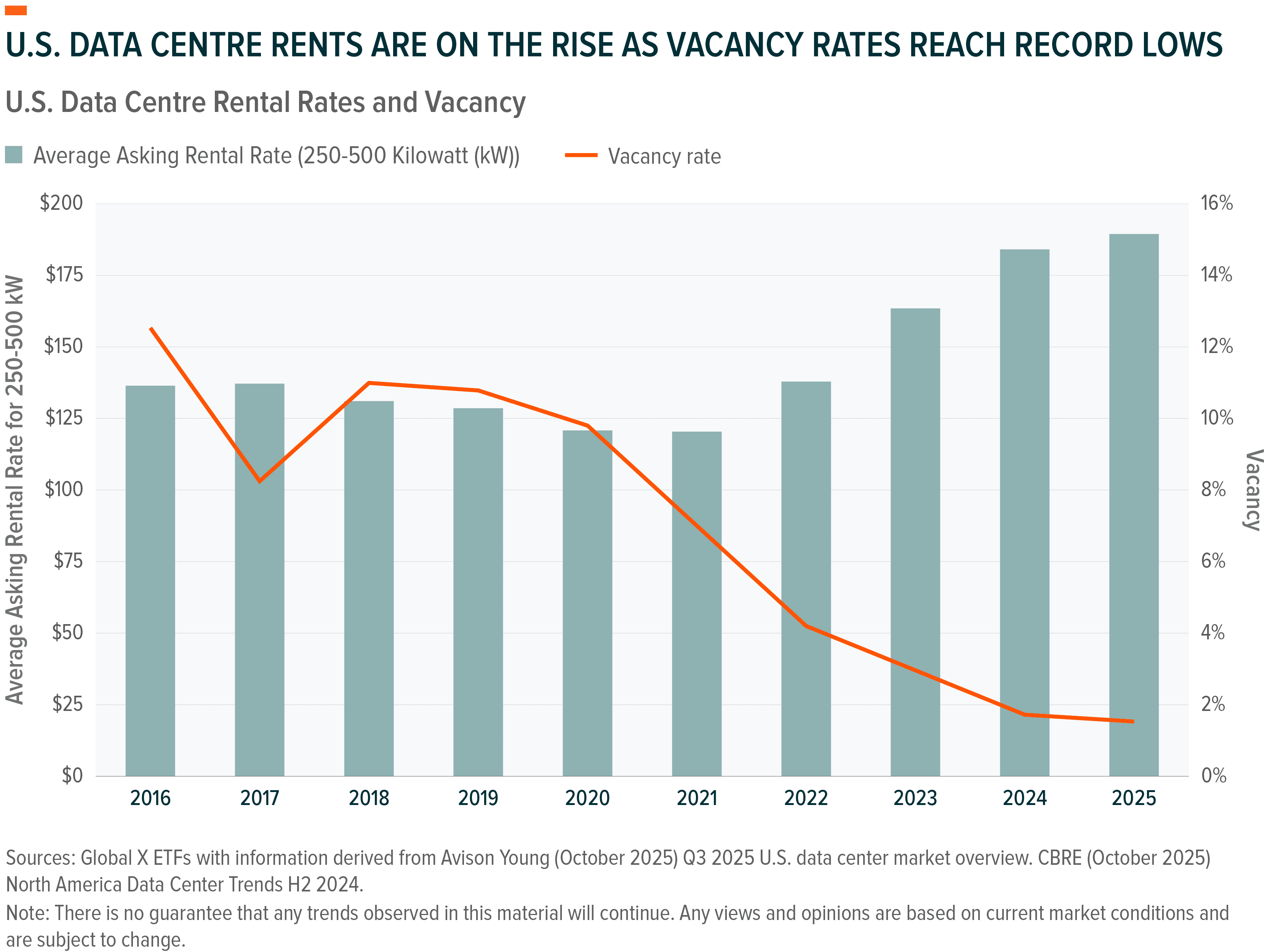

As demand for AI compute grows, U.S. data centre capacity appears to be reaching critical limits.20 Across most major U.S. data centre markets, vacancy rates are at historic lows.21 In Q1 2025, vacancy stood at just 1.6%, with key hubs like Northern Virginia operating even tighter.22 This trend persists even amid record breaking new construction activity in 2024, which saw nearly 7 GW of new capacity brought to market, twice that of the year prior.23 For context, new data centre absorption grew 34% YoY in 2024, after a 26% growth in 2023.24 Given the typical 12-18-month data centre development timeline, this imbalance is forecast by some to continue well into 2026.25

The scarcity of capacity could potentially create a powerful tailwind for incumbent operators. With few alternatives available at the scale and size that AI adopters require, customers might be less inclined to switch suppliers, keeping churn low and occupancy high. That could give data centre operators the upper hand when negotiating contract renewals, often locking in higher rents with minimal pushback.26 Rental rates had already surged to all-time highs by the end of 2024.27 Rising yields, which can indicate stronger pricing relative to development costs, may further enhance the advantage of scale, which larger operators can translate into better financing terms.28

Moreover, leading data centre operators typically structure multi-year leases with hyperscalers and large enterprises, often spanning 10 to 15 years.29 These agreements seem to support predictable earnings, particularly as clients become deeply embedded within specific facility ecosystems. This stickiness arguably reinforces the defensive growth profile of data centres.30

Data Centre Operators Race to Bring AI Projects to Market

As customer pipelines for AI capacity grows, some major colocation data centre operators are racing to scale and bring new capacity online.

AI Is No Longer Just a U.S. Story, It Is Going Global

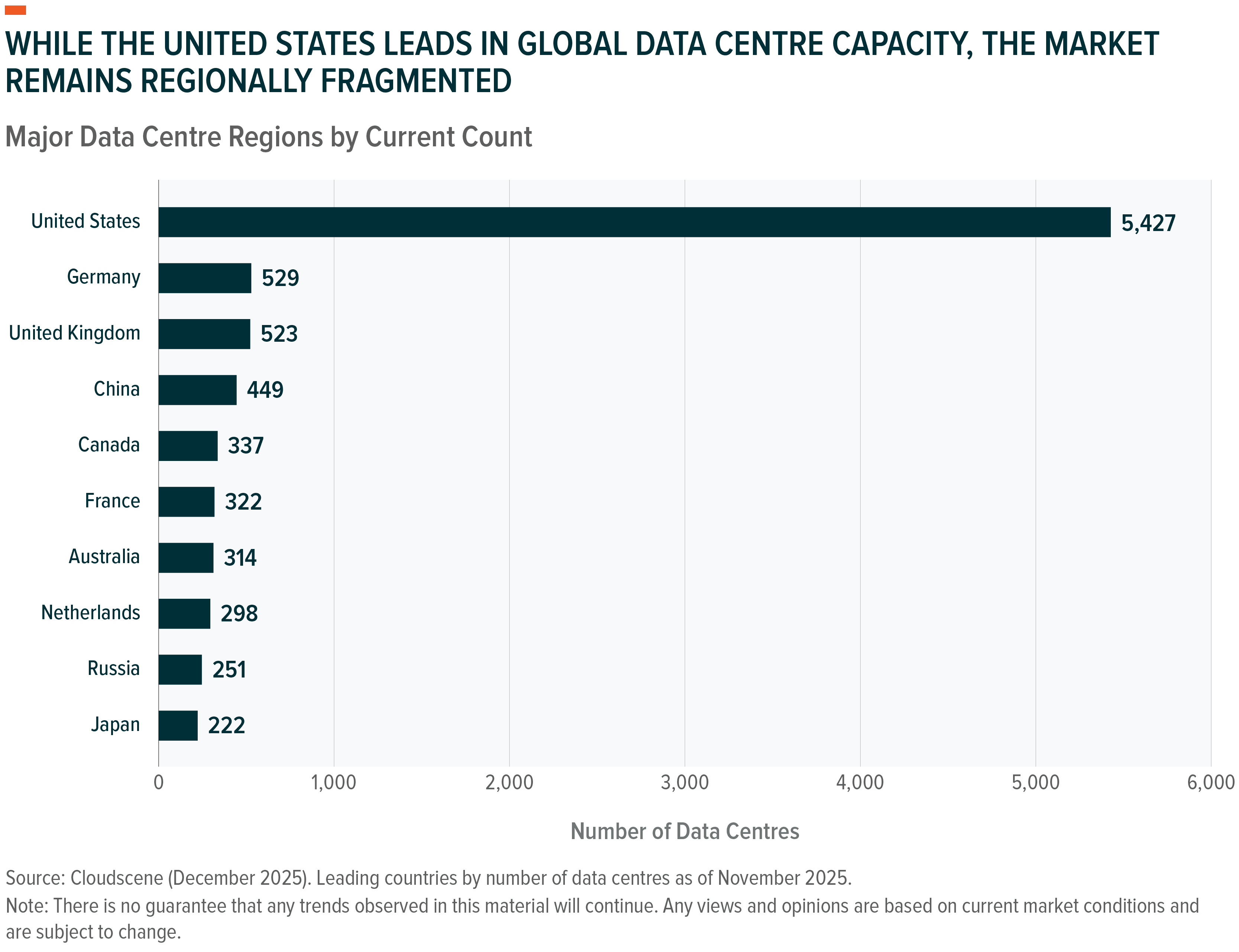

While the U.S. continues to lead in AI innovation35 - thanks in part to its dominance in semiconductors through companies like Nvidia - the data centre infrastructure story appears to be rapidly globalising.36

In China, open-source models like DeepSeek appear to have unlocked rapid deployment of AI at scale.37 Should enterprise and consumer use cases expand, infrastructure demands may grow in parallel. Power consumption from Chinese data centres alone may triple by 2030 to nearly 600 TWh, nearly twice that of the entire country of Indonesia.38

Regions like Europe also appear to be accelerating their AI infrastructure buildouts.39 Some estimates suggest that the EU is to absorb a record 937 MW of capacity in 2025, up 43% YoY, driven by sovereign AI efforts and regional digitisation strategies.40 Similar trends can be noted across other key regions, racing to bring new AI-data centre capacity online.41 Both Equinix and Digital Realty, two of the largest independent data centre operators worldwide, have scored many of their new deals in international markets this year.42,43

Worldwide, data centre power demand may grow to 945 TWh by the end of this decade, more than doubling from the total consumption at the end of 2024.44 The majority of this expansion is yet to be built. For investors, this potential and global dispersion could reinforce the opportunity for exposure beyond just U.S. hyperscalers.

VPN: Targeting the Long Tail of Digital Infrastructure Buildout

The Global X Data Center REITs & Digital Infrastructure UCITS ETF (VPN) is designed to provide targeted exposure to the companies powering the backbone of AI and next-generation computing. The fund seeks to track the Solactive Data Center REITs & Digital Infrastructure v2 Index, which emphasises depth, global reach, and thematic purity:

Additionally, the index ensures high thematic purity by requiring constituents to generate at least 50% of their revenue from the Data Centre or Cellular Tower-related sub-themes, which maintains a sharp focus on computing businesses.

Conclusion: Data Centre & Digital Infrastructure the Next AI Frontier?

Data Centres are becoming the checkpoint where every AI interaction must pass through., Data Centres are the utilities of the AI age. Computing needs could also expand aggressively from everyday conversational AI apps towards Physical AI and high-performance computing, such as those of Quantum Computing. Data centre operators who can bring capacity online quickly, and monetise it through their existing clientele and distribution, could potentially stand to benefit.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.

1. Data Centre News UK, When AI meets infrastructure: designing the data centres that can keep up, 20 November 2025

2. Ibid

3. Business Insider, ChatGPT is now being used by 10% of the world's adult population, 9 October 2025

4. Bloomberg, Inside AI’s rapid expansion: What investors need to know, 3 November 2025

5. Anglara, AI Use Cases by Industry: Real Examples Driving Results, 30 August 2025

6. Forbes, Top Infrastructure Upgrades Needed To Support AI And Quantum Growth, 5 August 2025

7. CBRE, Global Data Center Trends 2025, 24 June 2025

8. NAI 500, Why Data Center REITs and Stocks Are the Critical Infrastructure Play in the AI Era, 8 December 2025

9. Statinvestor. (n.d.). Information created globally 2005-2025. Accessed on July 15, 2025.

10. Gartner, Gartner Forecasts Worldwide IT Spending to Grow 7.9% in 2025, 2025, July 15

11. Mobile News, Millennials first into 5G fray following coronavirus pandemic, 9 October 2025

12. Yahoo Finance, The Shopping Shift: Consumers Turn to AI – Not Search Engines – to Shop Smarter and Faster, 1 December 2025

13. Google Cloud, “What is long context, and why does it matter?”, 21 November 2024

14. Bain & Company “How can we meet AI’s insatiable demand for compute power?” 22 September 2025

15. McKinsey & Company, “The cost of compute: A $7 Trillion race to scale data centres”, 27 April 2025

16. PRNewswire, Data Center Capex Surged 51 Percent to $455 Billion in 2024, According to Dell'Oro Group. 19 March 2025

17. CSIS, The Electricity Supply Bottleneck on U.S. AI Dominance, 2 March 2025

18. Pew Research Center “34% of U.S. adults have used ChatGPT, about double the share in 2023.” 25 June 2025

19. iMec, Agentic and Physical AI will change everything, 8 September 2025

20. Deloitte, 7 Shortages challenging AI data center expansion, 1 December 2025

21. Data Center Dynamics, Vacency rates in North America data centre markets hit record low, 11 September 2025

22. Avison Young. U.S. data center update, Q1 2025, May 2025

23. Slate AI, The AI-Driven Data Center Construction Boom, April 2025

24. Data Center Dynamics. Colo supply in primary data center markets increased by 34% in 2024, 7 March 2025

25. CSG Talent, Data Center Industry Trends 2026: Navigating Power, Sustainability, and Growth Challenges, 21 October 2025

26. Infrastructure Investor, Data Centres hold “golden ticket” to greater bargaining power, 3 October 2025

27. CBRE, Core Data Centre Markets Across the Globe Race to Increase Supply as Competition Heats Up, 26 June 2025

28. Chronograph, Infrastructure Private Equity: What You Need to Know, 9 June 2025

29. Infrastructure Investor, Data Centres hold “golden ticket” to greater bargaining power, 3 October 2025

30. Medium, “AI: How to Believe the Hype. Potential Boundaries of LLMs/GPTs” 23 November 2025

31. Equinix Investor Relations. Equinix Reports First-Quarter 2025 Results, 30 April 2025

32. Ibid

33. Nareit, Digital Realty Rides Secular Waves of Growth in its First 20 Years, 21 January 2025

34. S&P Global, Digital Realty, Equinix ramp up datacentres as AI drives demand, 30 June 2025

35. Medium, U.S. Secures Top Spot in Global AI Innovation Rankings, 22 November 2024

36. PwC, Unlocking the data centre opportunity in the Middle East, 10 April 2025

37. Silicon, Chinese Open-Source AI Shows Huge Rise This Year, 9 December 2025

38. Carbon Brief, Explainer: How China is managing the rising energy demand from data centres, 16 April 2025

39. EuroNews, European Investment Bank Group backs Commission's AI gigafactory plan, 4 December 2025

40. Tech Monitor, Europe’s data centre market to expand by 937MW in 2025 as demand surges, 14 February 2025

41. CBRE, Global Data Center Trends 2025 (24 June 2025)

42. Equinix Investor Relations, Equinix Reports First-Quarter 2025 Results, 30 April 2025

43. Digital Realty, Digital Realty Reports First Quarter 2025 Results, 24 April 2025

44. EA, AI is set to drive surging electricity demand from data centres while offering the potential to transform how the energy sector works, 10 April 2025