Europe

Loading...

Marketing Communication. Capital at Risk. Professional Investors Only. Please read fund legal documentation before making any final investment decisions.

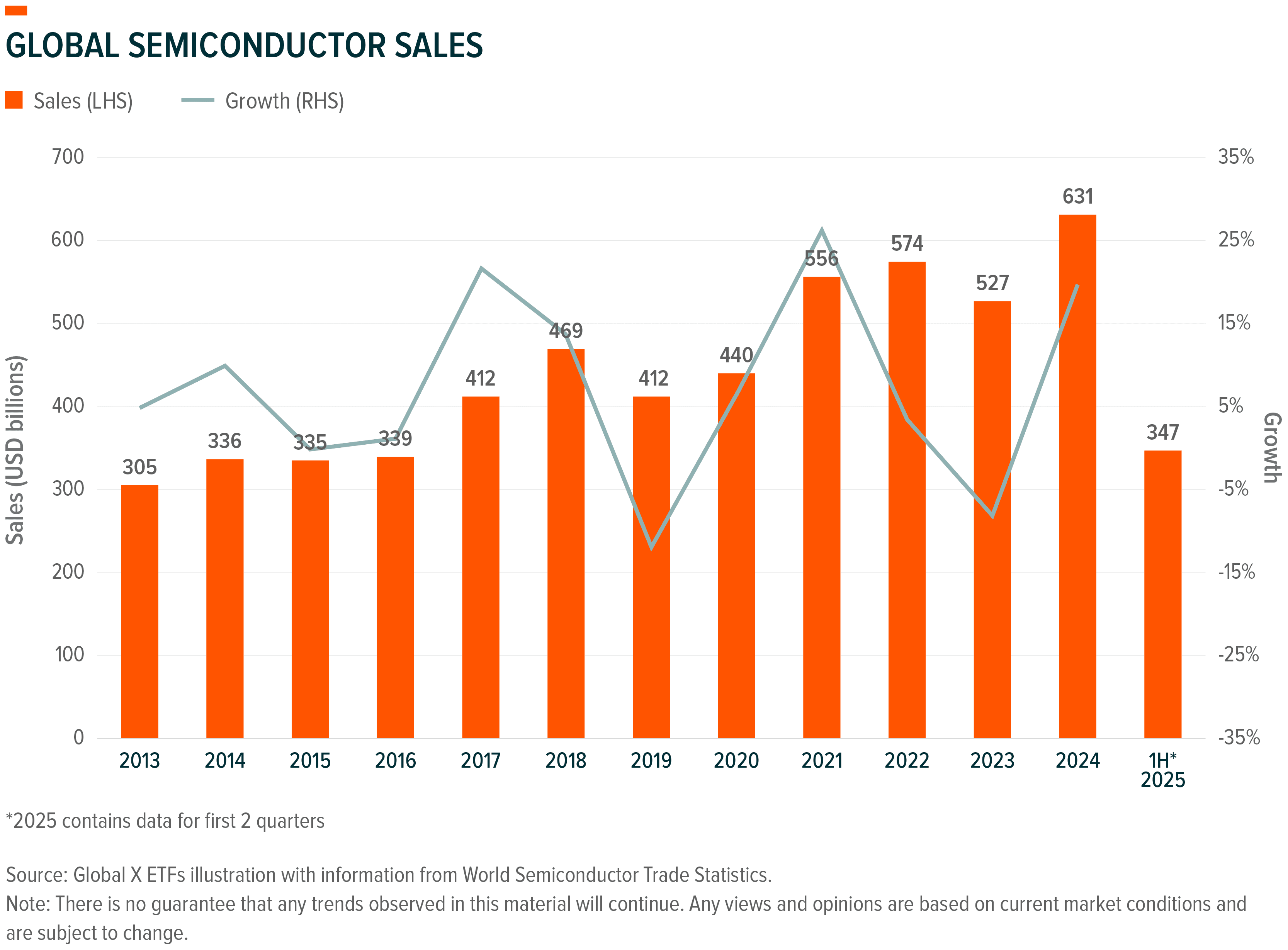

Semiconductors are the invisible backbone of the modern digital economy, driving everything from smartphones to data centres. Global chip sales have surged over the past decade, reaching an all-time high of $630 billion in 2024 despite a cyclical dip in 2023.1 This could approach $1 trillion by 2030, fuelled largely by new demand from artificial intelligence (AI) applications.2

This growth appears to mark a generational shift in computing needs. AI is reshaping the semiconductor industry, sparking a transition from general-purpose chips toward specialised “accelerator” processors and high-performance memory to handle AI’s data-intensity.3 Concurrently, governments are prioritising chip production through major incentives, reflecting how critical semiconductors are to economic and national security.4,5 Beyond today’s silicon, quantum computing is emerging as a breakthrough technology that could eventually tackle problems beyond the reach of classical computers.6 In short, the semiconductor sector could be on the cusp of a new era, with AI-centric chips powering near-term growth and quantum computing promising longer-term opportunities.

Key takeaways:

AI Semiconductors: The Engine Powering Next-Gen Applications

AI-oriented semiconductors, especially advanced processors like graphics processing units (GPUs) and AI accelerators, have become the chief engines of growth for the chip industry. Traditional central processing units (CPUs) are no longer sufficient for machine learning workloads, which require significant parallel processing.14 The breakthrough came in 2012, when researchers discovered GPUs (originally designed for graphics) could dramatically speed up neural network training.15 Since then, companies worldwide have raced to deploy AI-optimised chips in data centres to train large language models (LLMs) and other AI systems.16

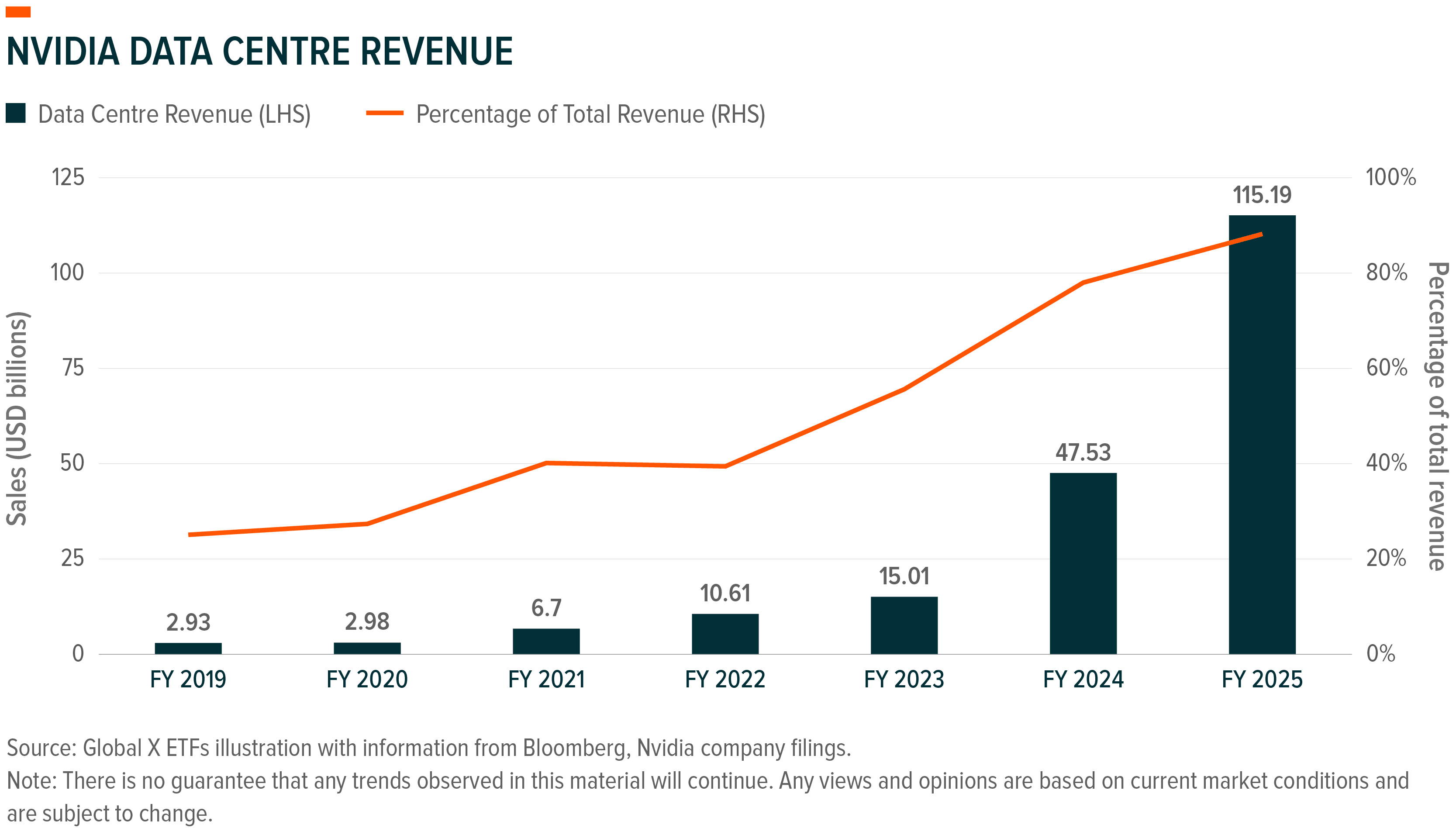

Arguably, it appears that no company has benefitted more from this trend than Nvidia, which today commands roughly 94% of the market for AI-centric GPUs.17 Demand for Nvidia’s AI chips has increased significantly alongside the rise of generative AI, so much so that its data centre segment has increased nearly 20× since FY21.18 The inflection point came with LLMs like ChatGPT, which required tens of thousands of GPUs running in parallel for training.19 This has driven unprecedented orders for high-end chips.20 Other tech giants have followed suit by developing their own custom AI chips (such as Google’s TPUs, Amazon’s Inferentia and Meta’s MTIA v1) to optimise specific AI workloads.21,22,23 The result is a structural shift: accelerator chips, from GPUs to custom ASICs, are displacing legacy general-purpose chips as the heart of modern computing.

The numbers illustrate how pivotal AI chips have become. Already, Big Tech firms are building out AI-optimised data centres, a wave of investment that could top $6.7 trillion by 2030, including $3.1 trillion on AI chips and infrastructure.24 Leading chipmakers have seen AI-related revenues soar. For example, Broadcom, which produces custom AI accelerators for cloud companies, reported its AI chip business grew 63% year-on-year to $5.2 billion in Q3 2025, its tenth consecutive quarter of growth.25

Notably, the supporting technologies around the processor have also become critical. AI systems require ultra-fast memory and networking to keep chips fed with data.26 High-bandwidth memory (HBM) is one example, enabling GPUs to keep their compute cores fully utilised and providing the data management needed to complete tasks efficiently.27 Global demand for HBM is projected to increase from about $4 billion in 2023 to over $130 billion by 2030, as advanced AI models require ever-greater memory bandwidth.28 Likewise, networking gear that links AI servers is also vital, with these systems designed to minimise latency and maximise bandwidth across racks and data centres.29 Even chip manufacturing is riding the AI wave, with foundries running at the cutting edge to produce these complex processors. TSMC noted that AI accelerator chip orders drove a significant revenue surge in 2024.30 In short, the AI-centric ecosystem, from cutting-edge GPUs to the specialised memory and interconnects they require, are powering the next generation of applications and, in the process, redefining the industry’s future.

Rising Demand Across Vertical Markets

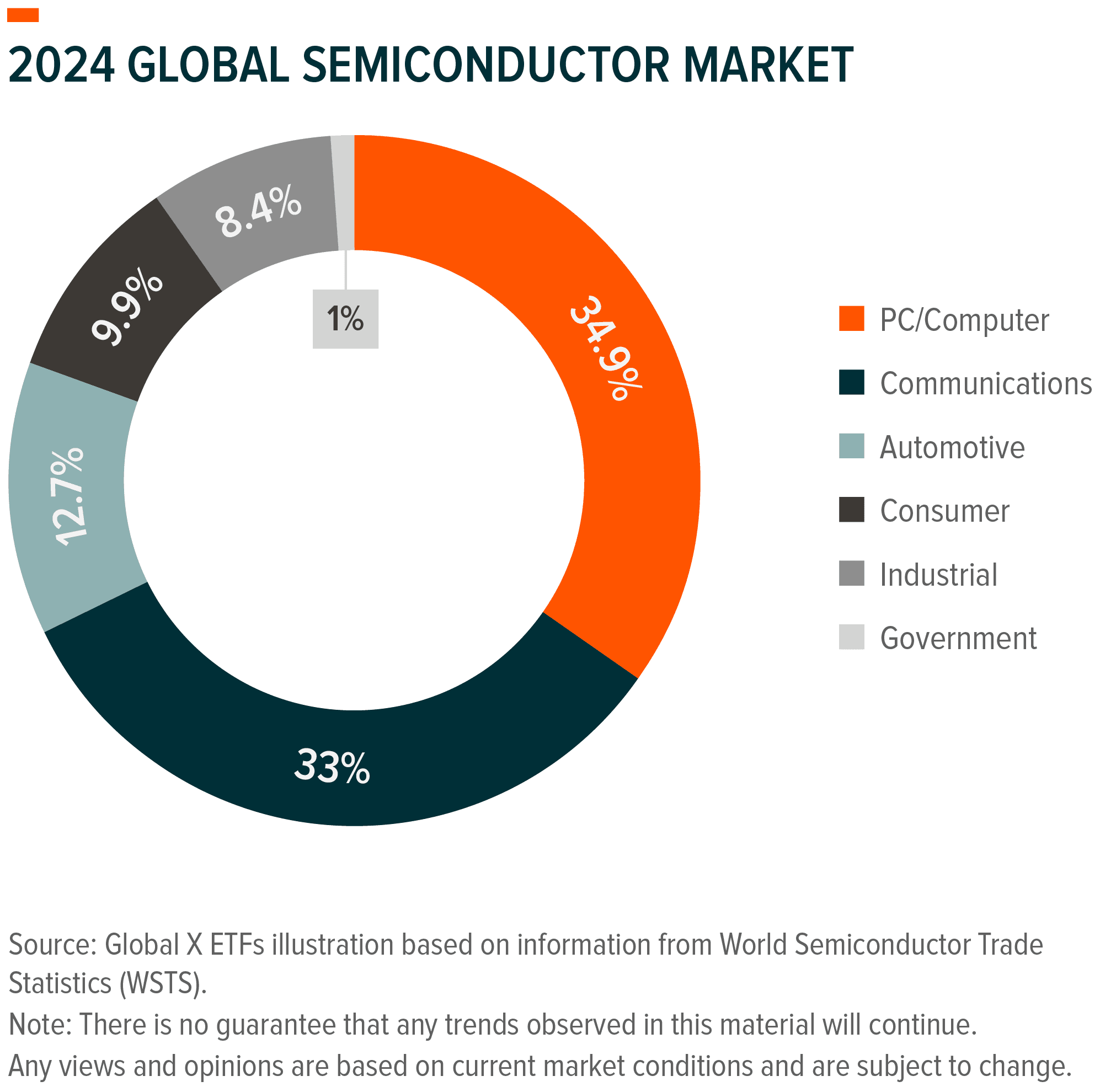

Importantly, the semiconductor upcycle isn’t confined to cloud and AI companies. Semiconductor demand is rising across a broad range of verticals, as more industries embed advanced chips in their products and infrastructure. Nowhere is this more evident than in the automotive sector.31 Cars have essentially become “computers on wheels,” equipped with semiconductors for engine management, safety systems, connectivity, and driver assistance.32 In 2023, the automotive market’s chip purchases grew so rapidly that it became the third-largest end market for semiconductors worldwide,33 a position it maintained in 2024.34 Modern vehicles now contain between 1,000 – 3,500 chips, and that number may only increase as electric vehicles (EVs) and autonomous driving features go mainstream.35 Notably, KPMG projects the automotive semiconductor market could exceed $250 billion by 2040, underscoring the long-term growth potential in this segment.36

Other sectors are following a similar trajectory. Industrial and manufacturing applications are adopting more sensors, controllers, and AI-enabled chips to enable smart factories and automation.37 The communications sector, which includes smartphones and telecom infrastructure, maintained a strong share of industry sales in 2024, partly due to 5G network rollouts and recovering smartphone demand.38,39 Despite declining in market share in 2023, traditional PC/computer demand rebounded in 2024, accounting for about 35% of chip sales in 2024.40 There, the mix appears to be shifting toward higher-value components such as processors and memory for high-end PCs and servers.41 Consumer electronics and government (including defence), make up the remainder of end-use demand.42

Crucially, these markets are increasingly interconnected.43 The rise of electric and autonomous vehicles, for instance, also drives demand for high-end logic chips (for AI driving algorithms), power semiconductors (for EV battery management), and connectivity chips (for vehicle-to-cloud communication).44,45,46 Industrial automation and smart city infrastructure lean on AI chips and sensors like those used in consumer devices.47,48 This breadth of demand bodes well for the industry’s resilience. It means the semiconductor sector’s growth is supported by multiple engines: not only cloud and AI, but also the digitisation of everything, from factories to vehicles and beyond.

Quantum Computing: Long-Term Complement to Classical Chips

While AI semiconductors drive current growth, a new computing paradigm is steadily maturing in research labs: quantum computing. Quantum computers operate on quantum bits (qubits) that can represent 0 and 1 simultaneously (through a property called superposition), unlike classical bits which are either 0 or 1.49 This seemingly esoteric difference enables quantum machines to handle certain complex problems with exponentially greater efficiency.50 For instance, tasks like simulating molecular interactions for drug discovery,51 optimising large-scale logistics,52 breaking certain cryptographic codes,53 or modelling climate patterns could be solvable with quantum computing.54 In short, quantum computing could hold the promise of tackling problems that are unsolvable for even the fastest supercomputers today.

It’s important to emphasise that quantum computers will not replace classical computers and AI processors for everyday computing – rather, they will complement them for specialised workloads.55 In practice, one can imagine future AI systems delegating specific optimisation or simulation sub-tasks to quantum co-processors, then incorporating the results back into classical pipelines.56 We are still some years away from that vision. As of 2024, quantum technology is very much in its infancy.57 The entire quantum computing industry generated less than $1 billion in revenue in 2024, as prototype systems are still limited in qubit count and error rates.58 Governments are not waiting on the sidelines – the U.S., EU, and China each have significant national quantum research programs aiming to spur progress.59,60,61

Gaining Exposure to the AI Semiconductor and Quantum Opportunity

The Global X AI Semiconductor & Quantum UCITS ETF (CHPX LN) is an index-based passive ETF that invests in pure-play computing technology companies that derive at least 50% of their revenues from the four key segments below:

The index employs a modified market cap–weighted approach, prioritising semiconductor leaders while capping individual holdings at 10% weight to preserve meaningful exposure to smaller, high-growth players across the AI semiconductor and quantum ecosystem. CHPX LN is global in scope, capturing both established and emerging semiconductor companies worldwide.

Conclusion

AI is driving a once-in-a-generation reset of the semiconductor industry. The rise of AI supercomputing hubs and the parallel development of quantum technologies expand the opportunity far beyond semiconductors alone. Specialised processors, high-bandwidth memory, and ultra-fast networking are becoming building blocks of next-gen computing. This shift, still in its early innings, could potentially influence trillions of dollars in computing infrastructure spending by 2030.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority.